SENSE INSIDER Personal Finance, Smart Investing & Budgeting Tips

SENSE INSIDER Personal Finance, Smart Investing & Budgeting Tips

You just started a new job, and HR needs a voided check to set up your direct deposit. Or maybe you wrote the wrong amount on a check and now you are staring at it, wondering what to do next. Either way, you need to know how to void a check, and you need to know fast.

The good news? It takes about 30 seconds once you know what you are doing. But if you skip a step or do it the wrong way, you could end up with a check that still looks usable, which creates a real security risk for your bank account.

In this complete guide, you will learn exactly how to void a check, when and why you would need one, what a voided check actually looks like, how to get one if you do not have a checkbook, and what to do if you already sent a check and need to cancel it. We cover all of it, whether you are in the US, UK, Canada, or Australia.

What Is a Voided Check?

A voided check is a paper check that has been marked so that it cannot be used to make a payment or withdraw money from your bank account. It looks like a regular check, but once the word “VOID” is written across it, no bank will process it as a payment.

Here is the key point: voiding a check does not destroy the information on it. Your bank routing number and account number are still fully visible at the bottom. That is actually the whole point. When you hand over a voided check to your employer or a service provider, they use those numbers to set up an electronic link to your account. Because the check itself is void, they cannot accidentally cash it.

Think of it like handing someone your house key to make a copy, but drilling a hole through the original so it cannot open your lock anymore. The information is still useful. The check itself is not.

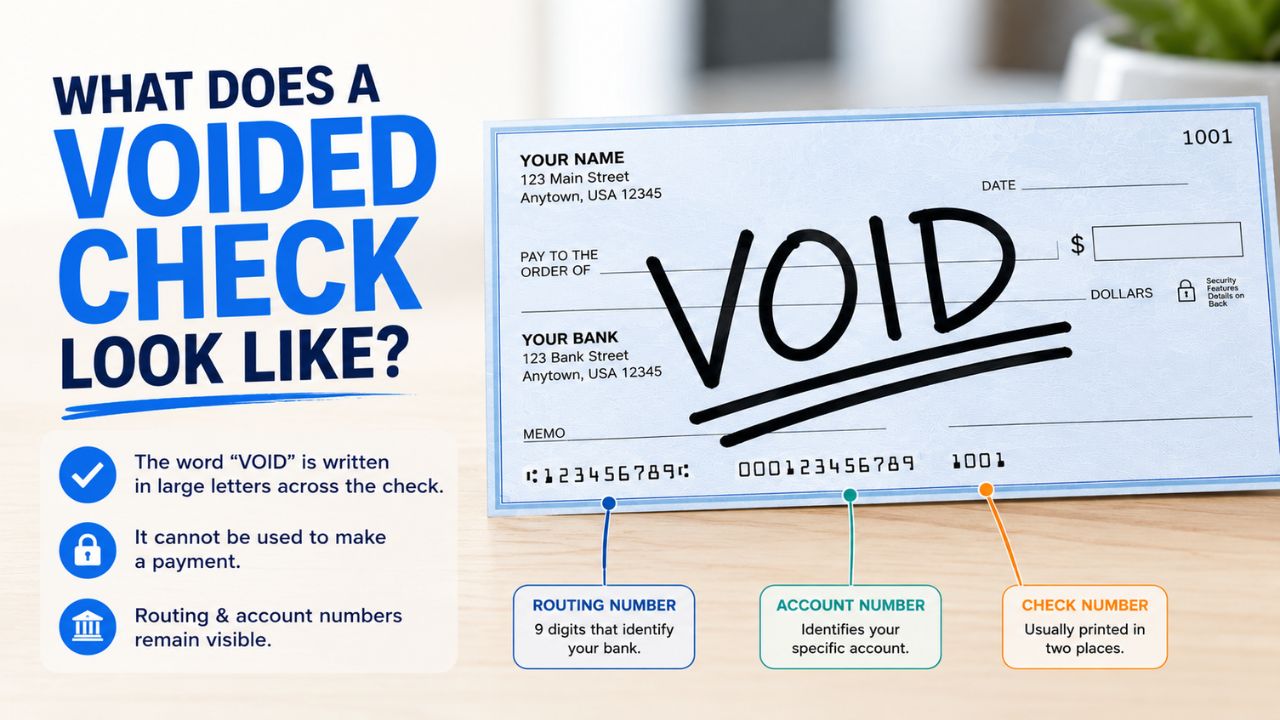

What Does a Voided Check Look Like?

A voided check example looks like a standard personal check with the word “VOID” written in large capital letters across the front. The writing should be big enough to cover most of the check face, especially the amount and signature lines, while keeping the routing and account numbers at the bottom clearly visible.

The numbers printed along the bottom strip of the check are what matter most:

- Routing number: A 9-digit number that identifies your bank

- Account number: The number that identifies your specific account

- Check number: Usually printed in two places on the check

These three pieces of information are what anyone setting up electronic payments, direct deposits, or automatic bill pay will need from you.

Why Would You Need to Void a Check?

Before jumping into the how, it helps to understand the why. There are several common situations where you would need a void check.

Setting Up Direct Deposit

This is by far the most common reason. When you start a new job or switch banks, your employer needs your banking details to deposit your paycheck electronically. A voided check is one of the fastest and most accepted ways to hand over that information securely.

Correcting a Writing Error

Made a mistake while filling out a check? Maybe you wrote the wrong dollar amount, misspelled the payee’s name, or put the wrong date. Rather than crossing it out or making the check look messy (which could get it rejected), you void it and start fresh with a new check.

Setting Up Automatic Payments

Subscription services, mortgage lenders, utility companies, and insurance providers often ask for a voided check when you want to set up automatic monthly payments directly from your checking account. It confirms your bank details before they initiate any transactions.

Setting Up a New Bank Account Link

Some financial apps, investment platforms, and money transfer services require you to verify a checking account by submitting a voided check or the account and routing numbers from one. This is how platforms like Venmo, PayPal, or your brokerage account can connect to your bank.

Record Keeping and Fraud Prevention

If you have leftover checks you do not plan to use, voiding them before storage or disposal prevents anyone from potentially using them. It is a small but smart security habit.

How to Void a Check: Step-by-Step Instructions

Here is exactly how to void a check properly. The process is simple, but each step matters.

Step 1: Grab a Blue or Black Ink Pen

Do not use a pencil. Do not use red or colored ink. You want a dark, permanent, non-erasable pen. A black gel pen is ideal because gel ink is resistant to chemical washing, a fraud technique where thieves use solvents to erase ink from checks and rewrite them. Brands like Uni-Ball specifically market anti-fraud pens for this reason.

Step 2: Write “VOID” in Large Capital Letters

Take your pen and write the word VOID in large capital letters across the entire front face of the check. Write it big enough that it clearly covers the payee line, the amount box, and the signature line. You want no one to mistake this for a valid check.

Some people write VOID multiple times across the check for extra security. That is completely fine and actually adds a layer of protection.

Step 3: Do Not Cover the Bottom Numbers

This is the one step people get wrong. While you want the VOID writing to be prominent, make sure it does not cover the routing number, account number, or check number printed along the bottom strip of the check. Those numbers are exactly what whoever asked for the voided check needs to see.

Step 4: Do Not Sign the Check

Leave the signature line completely blank. Signing a voided check can cause confusion and, in some edge cases, may create a legal grey area. Just leave it unsigned.

Step 5: Record It in Your Check Register

Write down the check number, the date, and note that it was voided in your checkbook register or wherever you track your checks. This helps you keep your bank records accurate and avoids confusion later during reconciliation.

Step 6: Deliver, Store, or Destroy It Properly

Once voided, either hand it over to whoever requested it, store it somewhere secure for future use, or destroy it completely by shredding it. Never just toss a voided check in a recycling bin or regular trash. Your account and routing numbers are still clearly visible, and that is sensitive information.

How to Get a Voided Check If You Do Not Have a Checkbook

Not everyone has paper checks anymore. If you do not have a checkbook, here are your options for how to get a voided check or a suitable alternative.

Request a Starter Check From Your Bank

Many banks will provide you with a small number of starter checks if you ask. Visit your branch or call customer service and explain what you need. Some banks will print or mail these at no charge.

Order a Check Book

If you do not have checks and want to have them on hand for future use, you can order a new checkbook through your bank’s online portal or by calling their customer service line. There is usually a small fee, and delivery takes a few business days.

Use a Voided Check Printout From Online Banking

Some banks, including Chase, Bank of America, and Wells Fargo, allow you to print a substitute voided check or an account verification letter directly from your online banking dashboard. Log in, look for something labeled “account information,” “direct deposit form,” or “get a voided check,” and follow the prompts. The resulting document includes your routing and account numbers and is accepted by most employers and financial institutions.

Provide a Direct Deposit Authorization Form Instead

Many employers and service providers will accept a direct deposit authorization form as an alternative to a voided check. You fill in your bank name, routing number, and account number manually. You can often get this form directly from whoever is asking for the voided check in the first place.

Use a Bank Verification Letter

Your bank can issue an official letter on their letterhead that confirms your account number and routing number. This is accepted in most situations where a voided check would otherwise be required.

Use a Counter Check

If your bank branch is nearby, you can often get a counter check printed on the spot. These are blank checks printed with your account information that you can then void and hand over as needed.

Void Check for Direct Deposit: What You Need to Know

Setting up a void check for direct deposit is one of the most common reasons people search for this topic, so let us walk through it clearly.

When you give your employer a voided check for direct deposit, here is what they do with it:

- They extract your routing number (identifies your bank)

- They extract your account number (identifies your checking account)

- They enter this information into their payroll system

- The payroll system uses these numbers to send your paycheck electronically via the ACH network (Automated Clearing House)

Your voided check itself gets filed away or discarded by your HR department. It is never processed through a bank. The only purpose it served was to confirm your banking details.

Pro tip: If you want your paycheck split between multiple accounts, such as a portion going to savings automatically, ask your employer if they allow split direct deposits. Many do, and you may need to provide a second voided check for each account you want money routed to.

For people in Canada, Australia, and the UK: the term “voided check” is primarily used in the US. In Canada, a “void cheque” works the same way. In the UK and Australia, you would more likely provide your sort code and account number directly, or use a bank verification letter, as paper checks are far less common in those banking systems. The concept of providing bank account details to set up direct payments is universal, even if the specific document looks different.

If you are working on organizing your finances beyond just setting up direct deposit, check out our guide to Smart Budgeting and Saving strategies that can help you make the most of every paycheck once it lands in your account.

How Do You Void a Check You Already Sent?

This is where things get more complicated. Once a check has left your hands, you can no longer void it in the traditional sense. You cannot write VOID on it because you do not have it anymore. Here is what you can do instead.

Request a Stop Payment

Contact your bank immediately, either by phone, through online banking, or in person at a branch. Ask to place a stop payment on the check. You will typically need to provide:

- The check number

- The exact dollar amount on the check

- The date it was written

- The payee’s name

Your bank will flag the check so that when it is presented for payment, it gets rejected. Most banks charge a stop payment fee, usually between $25 and $35, and the stop payment typically lasts for six months, after which it may need to be renewed if the check still has not been presented.

Stop payments are not guaranteed if the check is presented and processed before you make the request, but acting quickly gives you the best chance of stopping it.

Act Fast

Checks are usually processed within one to three business days of being deposited. If you realize you need to cancel a check, do not wait. Every hour counts.

Monitor Your Account

After placing a stop payment, keep a close eye on your bank account for the next few days to confirm the check did not go through before your request was processed.

Common Mistakes to Avoid When Voiding a Check

Even though voiding a check is simple, people make mistakes that create problems. Here are the ones to watch out for.

Covering the routing and account numbers. If your VOID writing covers those bottom numbers, the check is useless to whoever asked for it. You would have to void a second check. Always keep those numbers visible.

Using pencil or erasable ink. Pencil can be erased. Erasable pen ink can be removed with certain chemicals. Always use permanent ink.

Signing the voided check. There is no need to sign it. Doing so can cause confusion or in rare cases create unintended obligations.

Throwing it in the trash. A voided check still has your full bank account details on it. Shred it or destroy it if you are not handing it to someone or storing it securely.

Not recording it. If you use a check register, skipping the entry for a voided check can throw off your record keeping and cause confusion when reconciling with your bank statement.

Voiding the wrong check. Check numbers matter. If you void a check and enter the wrong number in your register, tracking your account later becomes messy. Double-check before writing.

Keeping Your Bank Account Secure When Using Voided Checks

Handing over a voided check means sharing your routing and account numbers with someone. That is sensitive information, and you should treat it accordingly.

Only provide voided checks to trusted entities. Legitimate employers, banks, financial apps, and utility companies all routinely ask for this information. But if someone you do not know or trust asks for a voided check for a reason that feels off, be cautious.

Be especially careful with job scams. A common fraud scheme involves fake employers asking new “hires” to provide banking information under the guise of setting up direct deposit, only to then use those details to drain the account or commit identity theft.

When in doubt, verify the identity of the company or individual requesting your voided check before handing it over. A quick search or a call to the company’s official phone number can go a long way.

Understanding how your banking information connects to your broader financial security is part of building a solid financial foundation. For a deeper look at the basics of managing your money well, our Personal Finance Basics section covers everything from banking fundamentals to retirement accounts in plain language.

FAQ: Common Questions About Voiding a Check

Can I void a check that has already been written but not yet sent?

Yes. If you have a completed check in your hands that has not been delivered yet, you can still void it. Write VOID across the front in large capital letters with a permanent ink pen. Record the check number in your register as voided and either file it or shred it.

Is a voided check the same as a cancelled check?

No. A voided check is one that has been manually marked as invalid before being sent to a bank. A cancelled check is one that has already been processed and paid by the bank. Banks often return cancelled checks to account holders as proof of payment, which is why “cancelled check” is sometimes listed as an acceptable document for certain legal or tax purposes.

What if I do not have any checks at all?

You have options. You can request starter checks or counter checks from your bank branch, order a new checkbook, use a direct deposit authorization form, or ask your bank for an account verification letter. Many banks also let you print a voided check substitute through their online banking platform.

How long is a voided check valid for?

A voided check does not expire in the traditional sense. Once it is voided, it stays voided permanently. However, if you are using a voided check to verify your banking details for direct deposit or automatic payments, the underlying account information (your routing and account numbers) remains valid as long as your account is open. If you close or switch accounts, you will need to provide updated banking details.

Can I void an electronic or digital check?

If a payment was initiated digitally, the process is different. You would need to contact the originating party (your employer’s payroll system, a vendor, etc.) directly to cancel or stop the payment. For ACH transfers specifically, you typically have a short window to request a reversal, usually one to two business days. Contact your bank immediately in these situations.

Conclusion: Voiding a Check Is Simple Once You Know the Steps

Voiding a check is one of those small but important financial skills that can save you a real headache when you actually need it. Whether you are setting up direct deposit at a new job, fixing a writing error, canceling a payment you no longer want, or just being proactive about keeping your unused checks from falling into the wrong hands, knowing how to do it correctly matters.

To recap: grab a blue or black permanent ink pen, write VOID in large capital letters across the front of the check without covering the bottom account numbers, skip the signature, record it in your register, and handle the finished check with care. That is genuinely all it takes.

If you do not have a checkbook, you still have plenty of options: online banking tools, starter checks, direct deposit forms, or a verification letter from your bank will all get the job done.

Got questions about how this fits into your broader financial picture? Explore more money management guides on SenseInsider to keep building smart financial habits one step at a time.

Disclaimer: This article is for informational purposes only and does not constitute financial or legal advice. Banking policies may vary by institution and country. Always confirm the specific requirements with your bank or the organization requesting your banking information.